What are scope 1, 2, and 3 emissions?

When it comes to carbon accounting, measuring greenhouse gas emissions inventory, and reporting on your carbon footprint, you’ll inevitably see the terms Scope 1, 2, and 3 emissions. But what do scope emissions mean? Why do they matter? And how do they impact your company’s carbon footprint?

This article provides an overview of the three scopes, so that you can confidently reference them in the context of GHG accounting.

How did Scope 1, 2, and 3 carbon emissions come to be?

Scope 1, 2, 3 emissions were developed by the Greenhouse Gas Protocol (GHGP), which is a global standard for measuring and managing climate-warming greenhouse gas emissions. Today the GHG Protocol, which is primarily led by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), supplies the world’s most widely used greenhouse gas accounting standards.

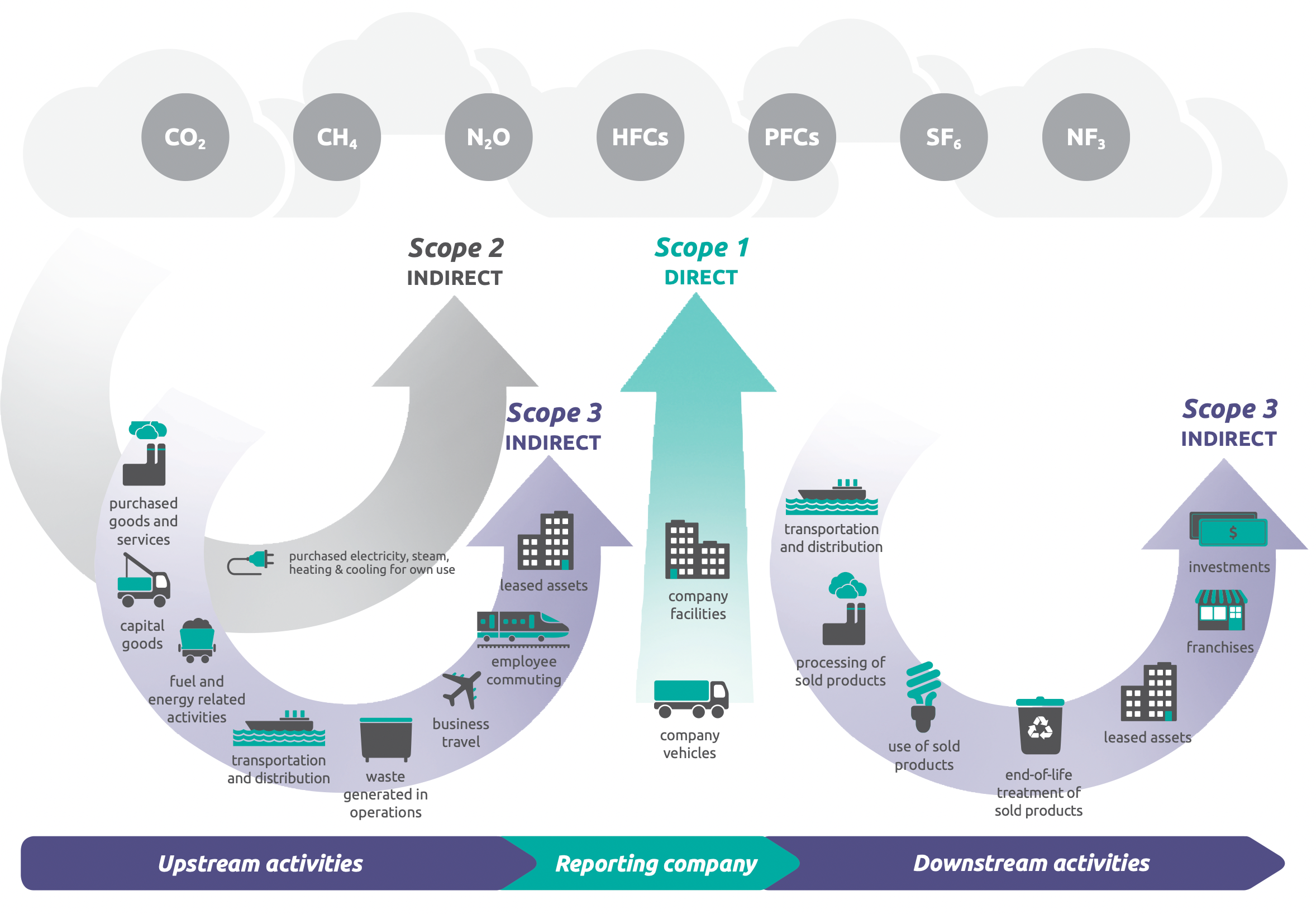

Since measuring an entity’s carbon footprint is complex, the GHG Protocol corporate standard breaks it down into three major “buckets” or scopes:

- Scope 1 — Direct Emissions

- Scope 2 — Indirect Purchased Energy Emissions

- Scope 3 — Indirect Value Chain Emissions

When added together, Scope 1 2 and 3 emissions give a reporting entity their total greenhouse gas emissions measurement. Keep reading to learn about the scopes in greater detail.

Scope 1 – Direct Emissions

Scope 1 consists of direct emissions from company-owned or controlled sources. Any ghg emissions created at or by company-owned facilities, equipment, and vehicles fall under Scope 1. Operations that are owned or controlled by a company directly fall under Scope 1.

One category of on-site activity that drives up Scope 1 emissions is Industrial Processes, which release emissions during on-site manufacturing. There’s an incredibly wide array of these production processes, and they can involve physical, chemical, electrical, and mechanical steps.

A second example is combustion, which is typically split into stationary and mobile combustion. Mobile Combustion is quite literally emissions caused by combustion for transportation. Even though electric vehicles are on the rise, most organizations still rely on the fuel combustion of diesel to powers their trucks and company-owned vehicles. And, as you might guess from the name, Stationary Combustion occurs in stationary, on-site locations and releases emissions when burning fuel for activities, like boilers and turbines.

Scope 1 emissions also include Fugitive Emissions, also known as “unintended” emissions. Fugitive emissions can be hard to track and often go unnoticed, but they’re critical to monitor because they typically involve potent greenhouse gases, like refrigerant gases, which are hundreds of thousands of times worse for the climate than carbon dioxide. For example, in the US, grocery stores leak an average of 25% of their refrigerants every year.

Scope 2 – Purchased Energy Emissions

These are indirect emissions generated from energy purchased or acquired by the reporting company. The most common type of Scope 2 emissions is purchased electricity (sometimes also called acquired electricity depending on how it’s paid for). But don’t forget, purchased energy can also include steam, heat, and cooling.

Nearly 40% of emissions come from energy generation, so Scope 2 emissions are a very important lever to manage when reducing emissions. One way to reduce your scope 2 emissions is to simply reduce your company’s energy consumption. Another way is to adjust the carbon intensity of your energy source.

Interestingly, a company’s Scope 2 emissions are highly dependent on how their energy is generated before it arrives on-site. For example, in California, 59% of electricity comes from renewable or zero-carbon sources; whereas, in Texas, 36% of electricity comes from renewables. That means, you can consume the same amount of purchased electricity in both states and have a lower carbon footprint in California.

Scope 3 – Value Chain or Indirect Emissions

For many companies, the majority of their emissions live outside of their direct operations. This is where Scope 3 comes into play. Scope 3 emissions are all of the other indirect emissions outside of purchased or acquired energy, which is measured in Scope 2. Commonly known as value chain or supply chain emissions, Scope 3 emissions are the indirect ghg emissions released by upstream and downstream partners in order to serve your business. In other words, they are the indirect emissions released by your company’s customers and suppliers in the course of their dealings with your company.

The GHG Protocol defines 15 unique categories within Scope 3 emissions:

- Purchased goods and services – All of the cradle-to-gate emissions of tangible or intangible goods and services purchased by the reporting company count here.

- Capital goods – Capital goods are often referred to as PP&E or fixed assets. They sometimes look similar to purchased goods, so companies need to make sure not to double count.

- Fuel- and energy-related activities – These are any remaining fuel or energy-related emissions not already counted in Scope 1 or Scope 2.

- Upstream transportation and distribution – Many organizations own or lease vehicles, but companies often use third-party transportation and distribution too. Those emissions count here.

- Waste generated in operations – What’s the volume of waste generated on-site? What does your waste disposal program look like?

- Business travel – How often are employees traveling for work? Do company employees use air travel?

- Employee commuting – Are employees walking to work, working from home, riding a bike?

- Upstream Leased Assets – Even if you don’t outright own operations, assets and equipment that you lease and use need to be considered in your Scope 3 emissions inventory.

- Downstream transportation and distribution – Emissions related to retail and storage of a products sold count here.

- Processing of sold products – If you sell to an intermediary (like a manufacturer) and your products are processed before being sold to the end user, then there are likely emissions caused by the processing of your sold products.

- Use of sold products – Some end products directly consume energy. For example, a lightbulb requires electricity to turn on and an airplane requires aviation fuel to fly. Other products indirectly require energy. For example, a t-shirt cleaned in a washer and dryer and a carrot stored in a fridge both indirectly required some energy use.

- End-of-life treatment of sold products – What happens to your products at the end of their life? Are they recycled? Are they compostable? Or do they end up in a landfill? This can be challenging to track, but counts here.

- Downstream leased assets – Unlike upstream leased assets, these are assets that you own but lease to others.

- Franchises – This is only relevant if you license out or operate a franchise model.

- Investments – Many businesses, even outside of financial institutions, make direct investments and those investments’s emissions are called financed emissions. When it comes to scope 3 emissions reporting, it’s important to measure the indirect impact of the investments that you support

Scope 3 emissions are important because they are a source of significant carbon emissions. The average company’s supply chain emissions are 5.5x higher than their direct emissions. Industrial supply chains alone are responsible for over 40% of all GHG emissions.

“Up to 90% of all total emissions are considered Scope 3.”

Scope 3 emissions are also complicated. Although 58% of Fortune 500 companies reported a plan to achieve net zero by 2050. Only a small group of those companies include Scope 3 emissions in those net zero plans.

What's the Difference between Upstream and Downstream?

It’s easy to get confused here. These terms refer to different parts of a company’s supply chain. Upstream activities are activities that bring inputs or materials closer to the reporting company. So for example, a restaurant’s upstream partner might be a farm providing arugula for salads. Downstream activities take a finished product away from the reporting company and closer to the end user.

How to Measure Scope 1, 2, 3 Emissions

Measuring your carbon footprint is the first step in any sustainability or ESG journey. Fortunately, Gravity can help you measure your Scope 1, 2, and 3 emissions with speed and ease. Carbon accounting doesn’t have to be stressful or time-consuming, and you don’t need to be an accounting expert.

Reach out to our team today to learn how we can help you measure your GHG emissions.